Wisdom for Investing

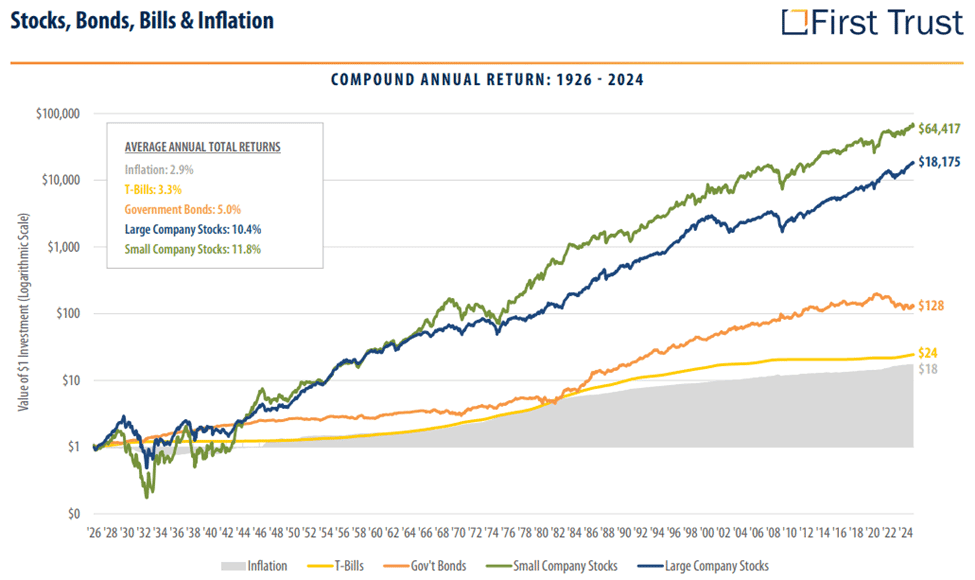

In client review meetings this year, we're spending some time discussing the strong results that bonds (fixed income) have produced in the past year while simultaneously acknowledging that inflation continues to be a drag on consumers worldwide. On the one hand, it is nice to get a return of between 6% and 8% from fixed income, particularly when they are much less volatile than stocks.

On the other hand, bonds have historically barely kept up with long-term inflation rates, and in many cases have had negative returns when accounting for inflation. So, when doing financial planning, we have to be extremely careful that we maintain your purchasing power over the course of your life. That often requires owning companies (stocks), as the below chart illustrates.

• $1 invested in 1926 would have grown to $24 in 2024 if it had been invested in a money market fund the entire time.

• $1 would have grown to $18 at the annual inflation rate over that 98 year period, so as stated above, you barely maintained your living standard over that time period.

• Alternatively, $1 grew to: $18,175 being invested in large US companies and $64,417 being invested in small US companies.

• Source: First Trust, as of 12/31/2024.

Two additional thoughts on inflation:

While the above data is the foundation for our views on planning for your long-term purchasing power, here are some additional thoughts on the topic:

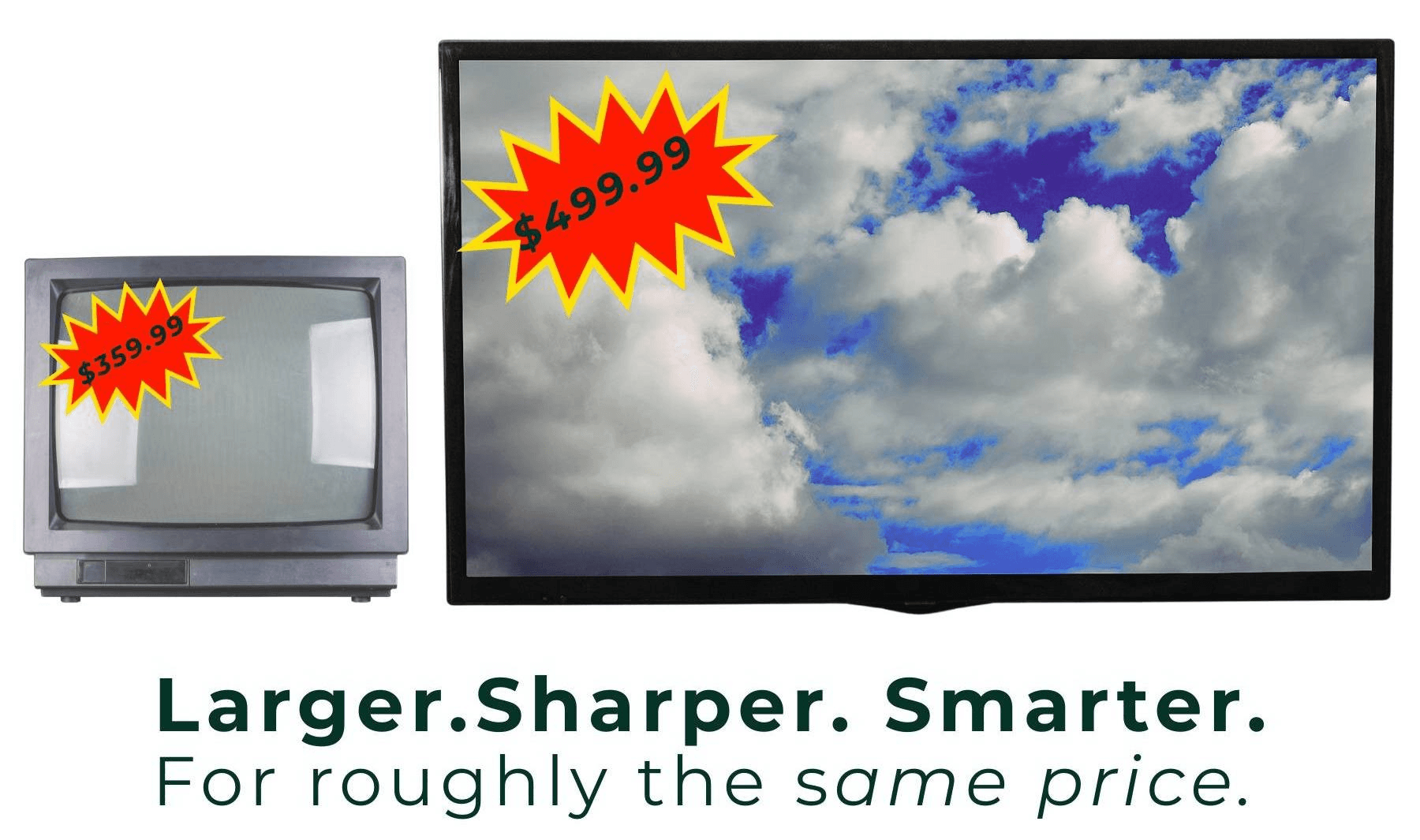

Technology has historically been disinflationary. Meaning, as technology progresses, prices (in certain categories) get pushed down.

Example: 25 years ago, the average television sold for between $500 and $700. Today, you can still get a TV for that price range, except it will be significantly larger, significantly higher resolution, and most likely have built in computing power so that it can access online applications. In summation, a significantly better product for the same price.

Another example: the original iPhone retailed for $499 in 2007. Adjusted for inflation, that is around $775 in 2025. As you may be aware, you cannot get an iPhone 17 pro for $775 today. Instead, it costs $1,099 for the base model, a 42% cumulative increase.

A 42% cumulative increase is noteworthy, but less so when you consider that it is estimated that the iPhone 17 lineup is 500 times more powerful than the original iPhone. (Source: TechRadar) Put differently, the overall value that the device delivers has grown significantly faster than its price tag.

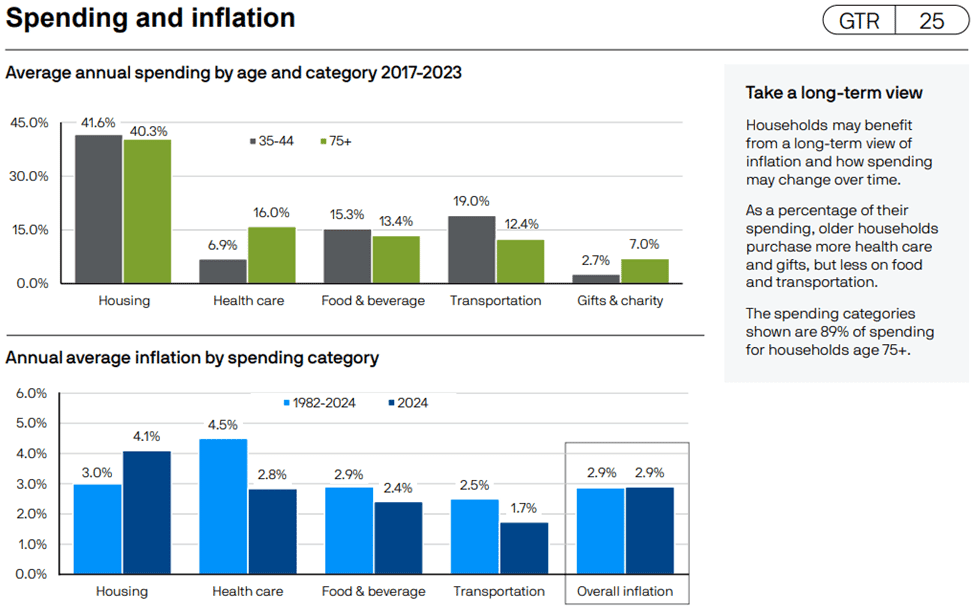

The rate of inflation experienced by retirees is different than other parts of the population. Meaning, most 80-year-olds do not travel as much as the average 50-year-old, so travel and leisure inflation rates have less of an impact on older individuals.

Per J.P. Morgan, health care spending accounts for 16% of spending for individuals over the age 75. Over the past 40+ years through 2024, health care inflation has averaged 4.5% growth per year.

Meaning, a medical expense that costs $5,000 today would cost $12,050 in 20 years. This is a prime example of what we're safeguarding against when we're constructing your investment portfolio to finance your spending through the entirety of your retirement.

Thanks for reading,

Jack O'Connor, CFP®